What QuantTwin Does

QuantTwin automatically learns mathematical models directly from financial data using Deep Learning.

- Learn market dynamics from historical data

- Estimate probabilities P(SN > K) and P(SN < K)

- Generate Monte Carlo scenarios

- Price European call and put options

- Risk analysis and stress testing

- Build AI-powered financial digital twins

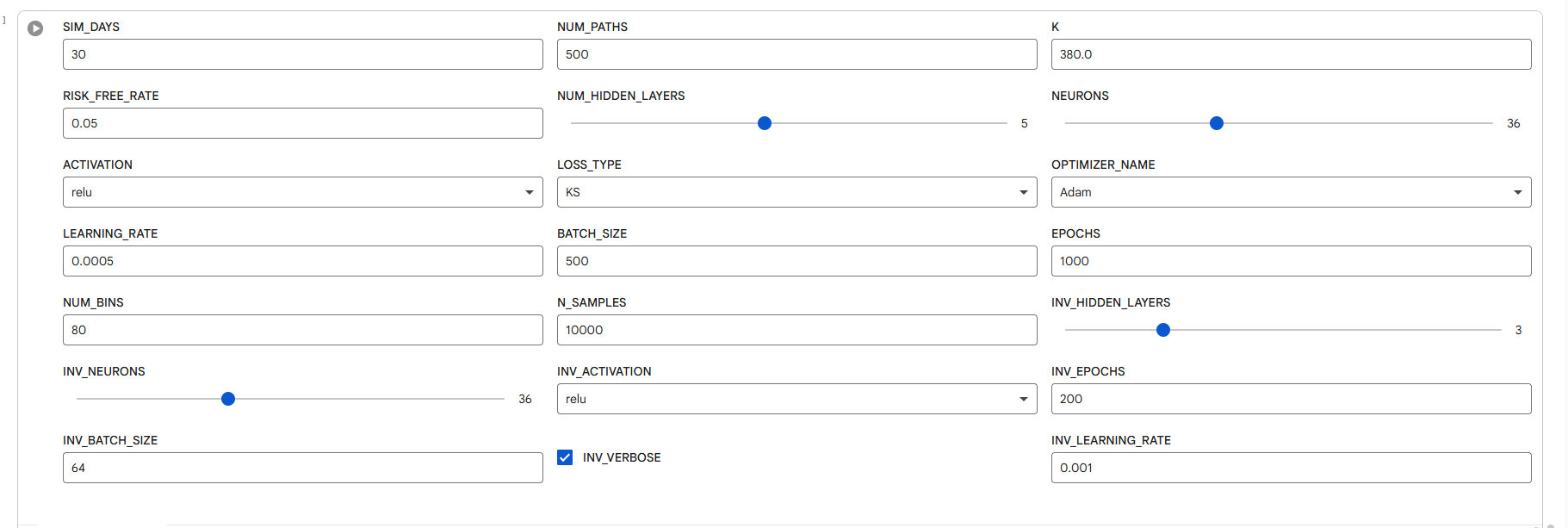

Platform Preview

A preview of the next-generation QuantTwin platform currently under development.

QuantTwin v1.0 Preview: Distribution learning, probability estimation, Monte Carlo simulation, option pricing, and AI-powered financial digital twins.

Upload financial data, learn market dynamics, estimate probabilities, generate Monte Carlo scenarios, and price derivatives from a single interface.

About the Founder

Dr. Ovidiu Calin

Professor of Mathematics

Eastern Michigan University

Author of Deep Learning Architectures – A Mathematical Approach

250,000+ downloads

Request Early Access

QuantTwin is currently under development.

Interested in a demonstration, pilot project, or institutional collaboration?

Contact QuantTwin